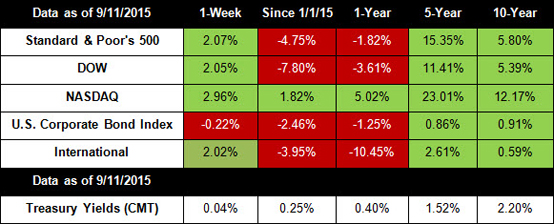

China's Growth Sputters

Fresh data out of China showed that factory output missed expectations, supporting the view that China's economic growth may dip below 7% for the first time since the global recession. Infrastructure investment also fell, leading many experts to believe that China's central government may be forced to roll out new measures to boost economic growth.[2]

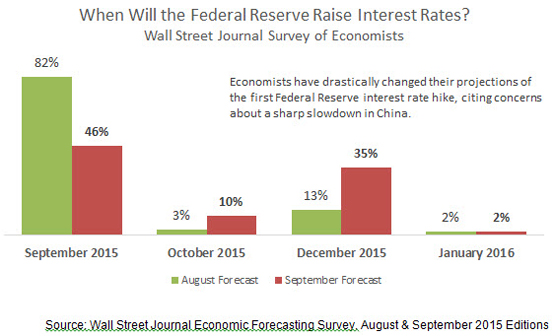

All Eyes on the Fed

This week, the eyes of the world will be on the Federal Reserve as the Open Market Committee votes on whether to raise interest rates for the first time in nearly a decade. The FOMC meets Wednesday and Thursday and will issue their official statement Thursday afternoon. The most recent Wall Street Journal survey of private economists shows that experts are split. Last month, a whopping 82% of economists thought that the Fed would pull the trigger this week; now, just 46% think the Fed will act this month.[3]

There are strong arguments to make on both sides of the issues. On the pro-rate-hike side are the opinions that too much easy money may fuel asset bubbles. Near-zero-rates also leave the Fed without ammunition in the event of another downturn.

On the hold-rates-steady side is the opinion that recent market volatility and ongoing concerns about global economic growth could spark another spate of selling if the Fed moves to raise rates now.[4]

Realistically, if the Fed moves this week to raise rates, they will likely announce a quarter-point raise to target interest rates in the 0.25%-0.50% range. How will markets react to a rate decision? It's hard to say. Investors might view an increase as a vote of confidence in the economy and rally. Alternately, sentiment might sour on fears of a new economic downturn.

With all the focus for the past six months on the Fed raising rates, it is finally down to the wire whether they're going to do something this week or not. As I have discussed previously, the longer they wait to raise the rates on the Fed funds, the more risk that will come into the markets. While a move this week could have a stabilizing effect for the short-term, longer-term the market still will be under pressure.

As I have discussed several times over the last week, we now have a secular downtrend as well as an intermediate downtrend with an upside ceiling on the market between the 2040/2060 levels on the S&P500. A failure to get above 1993.50 will suggest that the market will decline substantially over the next several weeks. The technical targets to the downside are for minimum move to 1780/1757. The intermediate levels to the downside suggests we could go to 1666/1610 over the next 8 to 14 weeks.

If we do trade up to the 2040/2060 levels, this will represent the right shoulder of the pattern suggesting the next move will be a minimum to the targets mentioned earlier at the 1780/1757 levels. There is still a 60% probability that the market will move below the 1867 lows made three weeks ago. Also there is a 60% probability that the lows at 1820 of the October lows of last year's will be penetrated. As always, we're keeping an eye on the situation and will update you as necessary.

ECONOMIC CALENDAR: Tuesday: Retail Sales, Empire State Mfg. Survey, Industrial Production, Business Inventories

Wednesday: Consumer Price Index, Housing Market Index, EIA Petroleum Status Report, Treasury International Capital

Thursday: Housing Starts, Jobless Claims, Philadelphia Fed Business Outlook Survey, FOMC Meeting Announcement, FOMC Forecasts, Fed Chair Press Conference

|